The Securities and Exchange Board of India Act or SEBI Act established a solid regulatory framework for the country’s growing securities markets. Henceforth, it has become the cornerstone of India’s capital markets, enabling SEBI to safeguard investor interests and foster a dynamic, transparent, and regulated securities industry.

The SEBI Act equips the regulator with extensive powers and duties and oversees a broad spectrum of activities in the securities markets. SEBI’s role, therefore, includes regulating market participants, enforcing disclosure mandates, and combating insider trading and market manipulation. This further ensures the integrity and stability of India’s capital markets.

Econometrics Tutorials with Certificates

Introduction to the SEBI Act

The Securities and Exchange Board of India (SEBI) Act, 1992, was passed by the Indian Parliament on April 4, 1992. Its main goal was to safeguard investor interests in the securities market. This Act also endowed SEBI with statutory powers, elevating it from a non-statutory entity to an autonomous body. Moreover, it falls under the administrative oversight of the Union Finance Ministry.

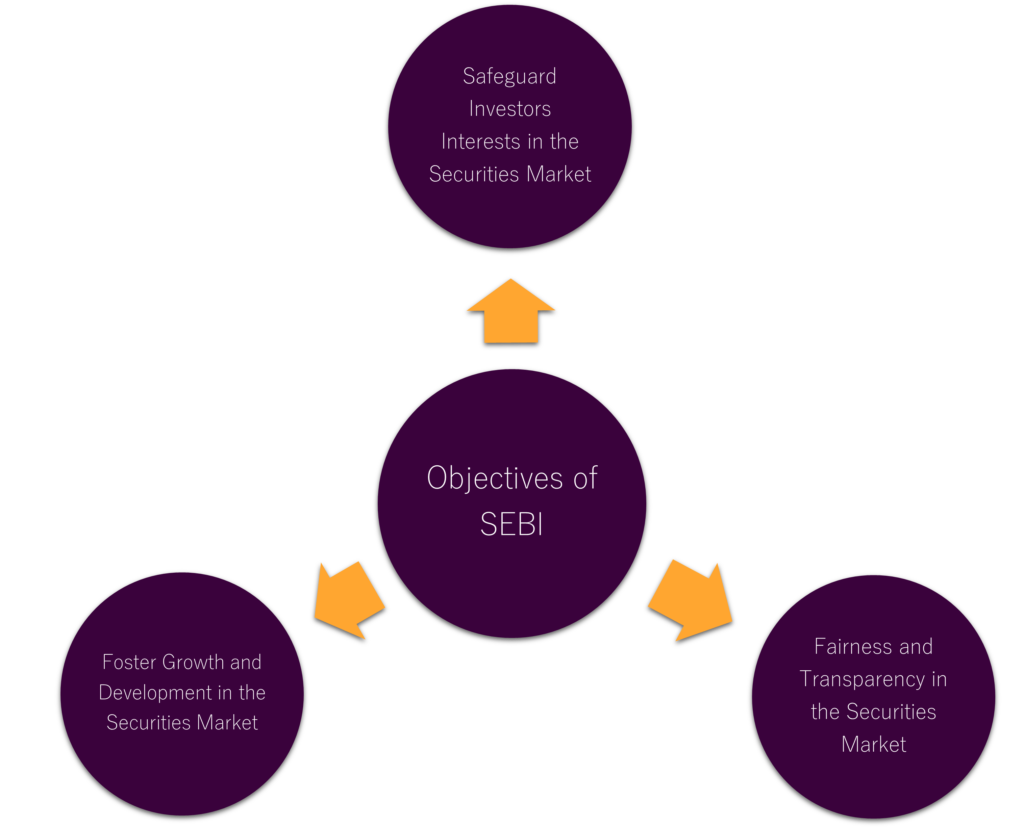

Purpose and Objectives of the Act

The SEBI Act’s primary objectives are:

- Safeguard the interests of investors in the securities market

- Ensure fair and transparent operations in the securities market

- Foster the growth and development of the capital markets in India

First, SEBI was established in 1988 as a non-statutory entity to oversee the securities market. It was formed through a Government of India resolution in the Department of Economic Affairs. The SEBI Act of 1992 was enacted, further granting it statutory powers and autonomy.

Composition and Management of the Board

SEBI’s core is its board, which includes a Chairman and several members. The board oversees SEBI’s overall direction and management and consists of:

- A Chairman, appointed by the Union Government of India

- Two members from the Ministry of Finance

- One member from the Reserve Bank of India

- Five other members, at least three of whom must be full-time members, appointed by the Union Government

Therefore, this diverse makeup ensures that SEBI’s decisions are informed by a range of perspectives. It also benefits from the expertise of government agencies and the financial sector.

SEBI’s headquarters is in Mumbai and it also has regional offices in major cities like Ahmedabad, Chennai, Delhi, and Kolkata. This extensive network allows SEBI to monitor and regulate the securities market nationwide.

The SEBI Act further empowers the organization with quasi-judicial, quasi-executive, and quasi-legislative powers. Hence, this enables SEBI to protect investor interests and promote the securities market’s orderly development.

Powers and Functions of SEBI

The Securities and Exchange Board of India (SEBI) stands as the pinnacle regulatory entity, overseeing the securities market regulation, investor protection, and corporate governance in India. Since its inception in 1988 and the grant of statutory powers in 1992, SEBI’s mandate has expanded. This adaptation also ensures the Indian capital markets’ evolving needs are met.

As the primary overseer of the securities industry, SEBI exercises a broad spectrum of powers and functions. These efforts aim to instill transparency, fairness, and efficiency within the market. Hence, SEBI’s key responsibilities include:

- Registering and monitoring market participants such as brokers, sub-brokers, and investment advisors.

- Issuing guidelines, regulations, and directions to govern the securities industry.

- Overseeing the activities of stock exchanges, mutual funds, and other financial intermediaries.

- Investigating and taking enforcement actions against market manipulations and unfair trade practices.

- Conducting investor awareness programs to educate and empower retail investors.

- Exercising quasi-judicial powers to adjudicate disputes and pass orders on securities law violations.

- Possessing quasi-legislative powers to make rules and regulations for the securities market.

- Implementing and enforcing securities laws and regulations through its quasi-executive powers.

As a result, SEBI’s multifaceted role as a regulator, protector, and facilitator has been pivotal in shaping a robust and dynamic securities market regulation framework in India.

Prohibition of Manipulative Practices

The SEBI Act of 1992 also establishes stringent measures to curb manipulative and deceptive tactics within the Indian securities market. These regulations are designed to uphold the market’s integrity and fairness. That is, they aim to eliminate practices that compromise ethical standards and erode investor confidence.

Insider Trading and Substantial Acquisitions

Insider trading, characterized by the use of material non-public information for personal gain, is strictly forbidden under the SEBI Act. The Act also governs substantial acquisitions of shares or control in publicly traded entities. Therefore, it mandates disclosures and adherence to takeover regulations.

Additionally, SEBI possesses the authority to investigate and enforce penalties against any violations of these prohibitions. The regulator’s dedication to upholding the law is evident through numerous high-profile cases:

- In 2017, SEBI imposed a fine of Rs.5,00,00,000 on Dipak Patel for engaging in front-running activities, resulting in a profit of around Rs.1,56,32,364.

- SEBI also levied fines of Rs.50,00,000 and Rs.40,00,000 on V. Narayanan and V. Natarajan, respectively, for creating fake accounts with exaggerated figures.

- In a notable case, SEBI banned Vijay Mallya from trading in securities and associating with listed companies for three years from June 2018 to May 2021. This was due to his involvement in manipulative activities through overseas accounts.

Financial Provisions and Auditing

The SEBI Act establishes a dedicated fund, the SEBI Fund, to be maintained and administered by the organization. This fund is essential for financing SEBI’s various activities. Moreover, it covers the payment of salaries and allowances to its officers and employees. It also covers the organization’s administrative and operational expenses.

To ensure transparency and accountability in SEBI’s financial management, the Act also mandates the maintenance of proper accounts. It further requires annual audits by the Comptroller and Auditor General of India. This rigorous auditing process serves as a crucial oversight mechanism. It scrutinizes SEBI’s financial records and ensures that the organization’s funds are being utilized effectively.

Penalties and Adjudication Process

Furthermore, the SEBI Act grants SEBI the authority to impose penalties for various infractions within the securities market. These penalties can include significant fines for not providing information, addressing investor complaints, or adhering to SEBI’s rules and regulations. The Act also outlines an adjudication process, enabling SEBI to conduct inquiries and impose monetary penalties on entities found guilty of offences. These offences further include insider trading, fraudulent and unfair trade practices, and failure to safeguard electronic databases.

Therefore, the SEBI Act outlines specific penalties for non-compliance, for example:

- Failure to furnish documents or reports: Not to exceed one lakh and fifty thousand rupees per failure.

- Failure to file returns or furnish information within the specified time: Not to exceed five thousand rupees per day of non-compliance under Section 15A(b).

The Securities Appellate Tribunal has also established a precedent that penalties should reflect the regulations in effect at the time of the violation. The Adjudicating Officer also considers several factors when determining the penalty. These factors include the disproportionate gain or unfair advantage made, the amount of loss caused to investors, and the repetitive nature of the default.

Appellate Tribunal and Legal Proceedings

The SEBI Act of 1992 further mandates the creation of a Securities Appellate Tribunal. Therefore, this entity is tasked with adjudicating appeals against Securities and Exchange Board of India (SEBI) rulings. The Tribunal’s composition includes a Presiding Officer and members with expertise in law, finance, and securities markets.

As a result, individuals dissatisfied with SEBI’s verdicts can appeal to the Securities Appellate Tribunal. This body possesses the authority to issue orders and judgments, therefore, addressing grievances and ensuring the securities market’s integrity. The Act delineates the Tribunal’s jurisdiction, authority, and procedural framework, establishing a solid legal structure for investor appeals.

Conclusion

Thus, the SEBI Act of 1992 has been a transformative force in India’s securities markets. It also established SEBI as an autonomous authority, crucial for investor protection and market fairness. Hence, this legislation has been instrumental in the growth of India’s capital markets.

SEBI’s role is multifaceted, encompassing market monitoring, regulation enforcement, and stability maintenance. The Act’s comprehensive framework has solidified its position as a cornerstone of India’s financial regulation. Moreover, it has significantly contributed to the securities industry’s growth and maturity.

SEBI’s importance in India’s financial landscape is evident in its regulatory, developmental, and supervisory functions. Its dedication to investor education and compliance has fostered confidence. As a result, it has been pivotal in the securities market’s development.

Econometrics Tutorials with Certificates

This website contains affiliate links. When you make a purchase through these links, we may earn a commission at no additional cost to you.