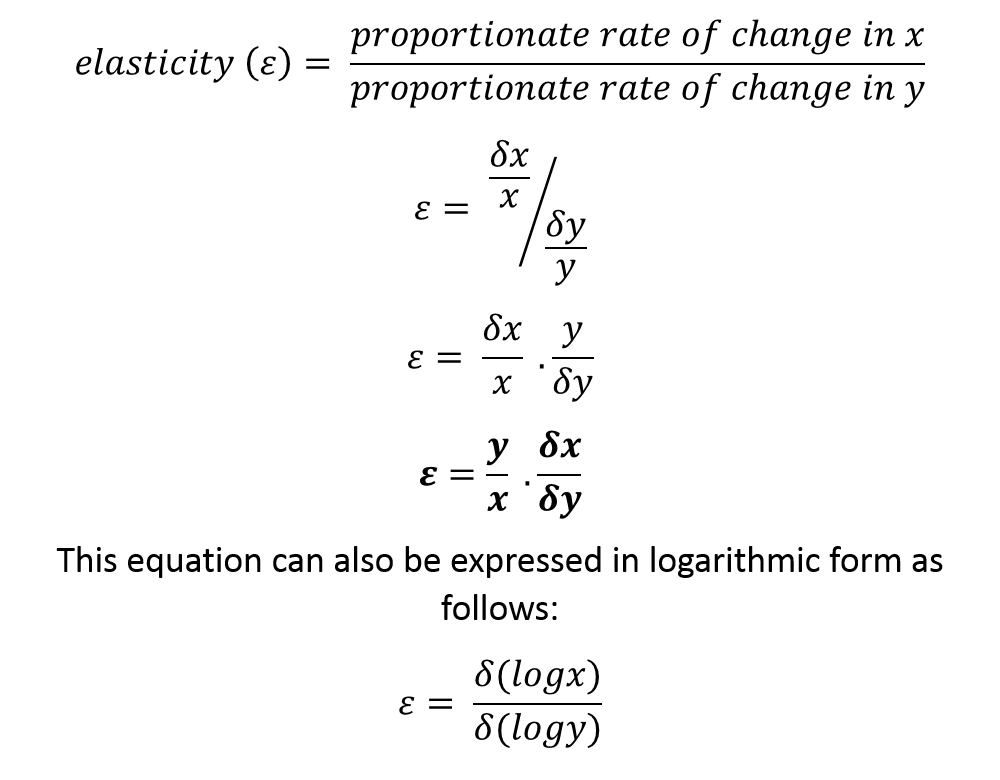

In economics, the concept of elasticity holds special significance. Economists deal with various types of elasticity such as price or income elasticities of demand. In many cases, it is preferred to estimate the elasticity of variables instead of absolute changes. This is because elasticity is not affected by units of measurement.

Elasticity refers to the ratio of the proportionate rate of change in one variable and the proportionate rate of change in another variable. It is often used to measure the sensitivity or degree of responsiveness of one variable in response to changes in another variable. Also, it can be defined as the percentage change in one variable as a result of a one per cent change in another variable.

Let us consider 2 variables ‘x’ and ‘y’. The elasticity of ‘x’ in response to changes on ‘y’ can be expressed as:

The elasticity is sometimes estimated using the logarithmic form in the regression approach. It is easy to apply using Ordinary Least Squares (OLS) by converting the variables into log-from.

Econometrics Tutorials with Certificates

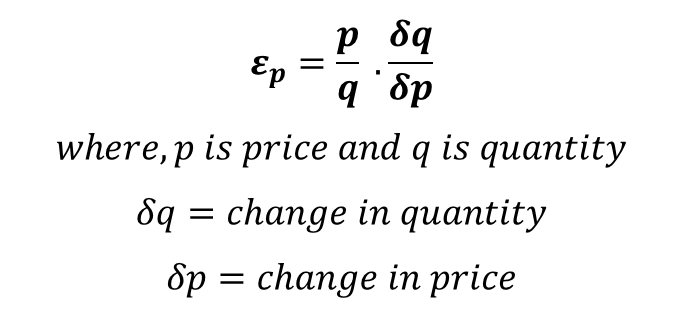

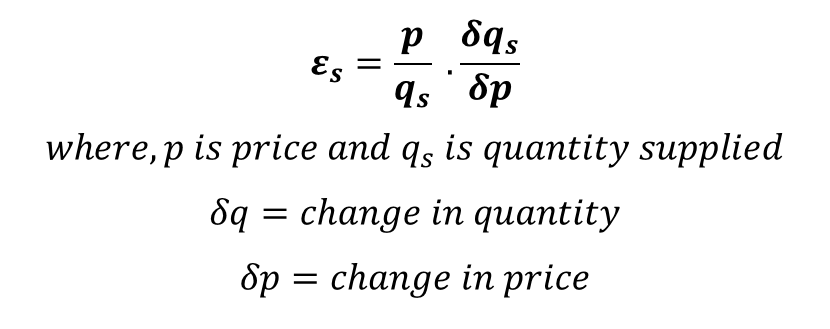

Elasticity of demand: Price Elasticity

Price Elasticity of Demand

Price elasticity of demand can be estimated as the proportionate rate of change in quantity demanded of a commodity divided by the proportionate rate of change in its price. In terms of percentage, it is defined as the percentage change in quantity demanded as a result of a one per cent increase in the price of the commodity.

According to the law of demand, price and quantity have a negative relationship. With a rise in price, the quantity demanded of a commodity falls. Hence, the demand curve is usually a downward-sloping curve.

Due to this negative relationship, the price elasticity of demand is a negative number. However, we are usually interested in the magnitude of elasticity which can be estimated by taking the absolute value of elasticity. Therefore, the negative sign is mostly ignored.

Types of Price Elasticity

Depending on the value of Elasticity, price elasticity of demand can be 5 types:

| Type | Value of Elasticity | Meaning |

| Perfectly Elastic Demand | E = infinity | Consumers demand an infinite quantity of a commodity. They are willing to buy the entire quantity of commodity available at the given price. But, with even a slight increase in price, the demand will fall to zero. Here, the demand curve is horizontal and parallel to the x-axis. |

| Perfectly Inelastic Demand | E = 0 | Irrespective of the price of the commodity, the quantity demanded by consumers is constant. Therefore, a rise or fall in price has no effect on how much commodity consumers will buy. The demand curve is vertical and parallel to the y-axis. |

| Unitary Elastic Demand | E = 1 | The proportion of the rise in price is equal to the proportion of the fall in quantity demanded. In this case, elasticity is said to be unitary elastic. For example, elasticity is unitary elastic if a 10 per cent fall in price leads to a 10 per cent rise in quantity demanded. |

Elastic and Inelastic Demand

| Type | Value of Elasticity | Meaning |

| Elastic Demand | E > 1 | Demand is said to be elastic if the percentage change in quantity demanded is greater than the percentage change in price. For example, a 10 per cent rise in price causes a 15 per cent fall in quantity demanded. Then the elasticity of demand for that good is referred to as elastic. This is usually true for goods that are not required for survival or goods that are not considered to be a necessity. Therefore, consumers can easily substitute these commodities for other goods. Goods that have high elasticity are usually called luxuries. |

| Inelastic Demand | E < 1 | The percentage change in quantity demanded is less than the percentage change in price. The price elasticity of demand is considered to be inelastic in such cases. For instance, a 10 per cent rise in price leads to a 5 per cent fall in quantity demanded. In the case of necessities, demand is usually inelastic because a certain quantity of these goods must be purchased by consumers irrespective of their price. Therefore, even if the price of such goods rises, the fall in their demand is usually less than proportionate. |

Factors affecting Price Elasticity

- Substitutes: price elasticity of demand is usually higher for goods that have many substitutes as compared to goods with no substitutes. This is because consumers can easily switch to other substitute goods if the price of the commodity rises. For a commodity that has no substitute, consumers do not have any options for alternative goods in case the price of the good increases.

- Tastes and preferences: strong preferences for a commodity lead to inelastic demand. Brand loyalty and consumer habits play a huge role in building up tastes and preferences. This leads to relatively inelastic demand as compared to goods that have no preference among consumers.

- Type of commodity: as discussed earlier, the nature of a good affects its elasticity. Necessities tend to have inelastic demand because these commodities are considered necessary by consumers. Whereas, demand for luxuries is usually more elastic as consumers can easily stop buying such commodities.

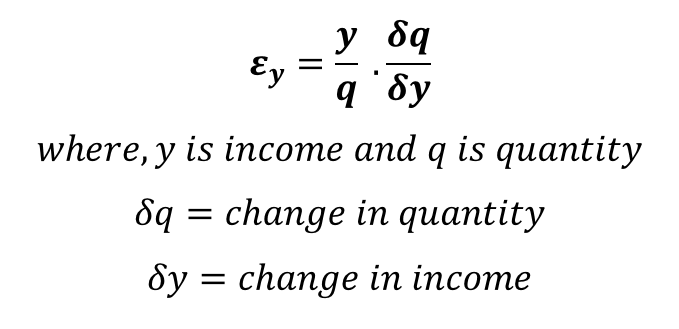

Income elasticity of demand

Income elasticity shows the responsiveness of the quantity demanded of a commodity with changes in the income of the consumer. It can be calculated as the proportionate rate of change in quantity demanded of a commodity divided by the proportionate rate of change in income of the consumer. It can also be defined as the percentage change in quantity demanded of a good as a result of a one percent increase in the income of consumer.

Types of Income elasticity

Positive Income elasticity (Normal goods): normal goods have a positive income elasticity. This implies that an increase in the income of consumer leads to a rise in the quantity demanded. Conversely, a fall in income causes a fall in the quantity demanded of that good. The increase or decrease may be elastic, inelastic or unitary elastic.

Negative Income Elasticity (Inferior goods): in cases of certain goods, the income elasticity may be negative. This happens because the consumers start to prefer other goods as their income and status of living rise. Hence, a rise in income leads to a fall in the quantity demanded of such goods. These goods are referred to as inferior goods.

Zero Income Elasticity: this refers to a situation of no relationship between quantity demanded of a commodity and income of the consumer.

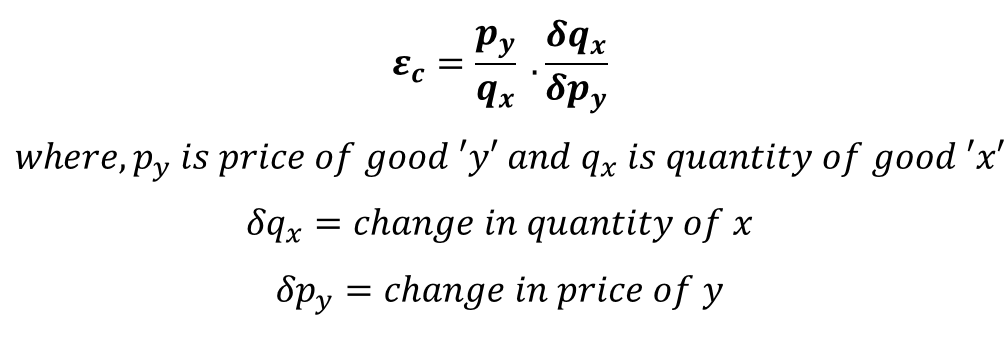

Cross elasticity of demand

A proportionate rate of change in quantity demanded of one commodity due to the proportionate rate of change in the price of another commodity is known as the cross elasticity of demand. It helps determine the nature of the relationship between two goods. It can also be defined as a percentage change in quantity demanded of good ‘x’ as a result of a one percent increase in the price of good ‘y’.

Types of Cross elasticity

Positive Cross Elasticity (substitutes): For substitute goods, the cross elasticity of demand is positive. With an increase in the price of one good, the quantity demanded of the other good increases and vice versa. This happens because the good with a higher price is substituted by the consumers. And, consumers start buying the good that has become relatively cheaper

Negative Cross Elasticity (complements): In the case of complementary goods, the relationship is reversed. A negative relationship arises between the price and quantity of complementary goods. With an increase in the price of one good, the quantity demanded of other good falls. This happens because both the goods are used together. A rise in the price of one leads to a fall in the demand for both goods.

Zero Cross Elasticity: In such a case, the goods are neither substitutes nor complementary. There is no relationship between the given commodities.

Elasticity of supply

Similar to price elasticity of demand, the concept of elasticity is also applicable to supply. It is defined in the same way as the proportionate rate of change in quantity supplied of a commodity divided by the proportionate rate of change in the price of that commodity. In terms of percentage, it is the percentage change in quantity supplied of a commodity with a one percent increase in its price.

Opposite to the law of demand, price and quantity have a positive relationship here and the supply curve is generally upward sloping. Therefore, the price elasticity of supply is usually a positive number because price and supply move in the same direction.

Types of Elasticity of Supply

| Type | Value of Elasticity | Meaning |

| Perfectly Elastic Supply | E = infinity | It refers to an infinitely elastic supply curve where producers supply the entire commodity available at the given price. But the supply falls to zero with even a slight change in price. The supply curve is horizontal to the x-axis. |

| Perfectly Inelastic Supply | E = 0 | In this case, the supply curve is vertical. It generally occurs for rare goods with a finite quantity or in the short run for some commodities. Rare goods like antiques and commodities like agricultural products in the short run can have a vertical supply curve. |

| Unitary Elastic Supply | E = 1 | A percentage change in price is accompanied by an equal percentage change in quantity supplied. The elasticity of supply is said to be unitary elastic in such a case. |

| Elastic Supply | E > 1 | The percentage change in quantity supplied is greater than the percentage change in its price. |

| Inelastic Supply | E < 1 | Inelastic supply is one where the percentage change in quantity supplied is less than the percentage change in its price. |

Determinants of Elasticity of Supply

Production costs

Variations in production costs with changes in output play an important role in determining the elasticity of supply. Supply will tend to be more elastic with higher variations in production costs. Suppose, if a slight increase in output leads to a huge rise in production costs, sellers will prefer to shift their production to other commodities. Hence, the elasticity of supply will be higher with higher elasticity of costs of production.

Time period

Supply of certain goods, especially agricultural goods, is inelastic in the short run. It can only be adjusted over a longer period of time. Even in the case of durable goods or goods that can be quickly produced, short-run supply tends to be relatively inelastic. This is because producers have more opportunities for expansion and improvement of technology in the long run to increase supply.

Type of commodity

Durable goods can be stocked up and their supply can be readily increased or decreased with adjustments in their price. However, perishable goods have a relatively inelastic supply because they cannot be hoarded or stored for a long period of time. Additionally, certain rare goods such as antiques are finite, implying that their supply cannot be increased or decreased.

Nature of inputs

Supply of a commodity can be varied if inputs or factors of production are available. The supply of a commodity will be inelastic if factors of production are not easily available. That is, if supply of inputs required for production is inelastic, the supply of the commodity will also be inelastic.

Expectations

If producers expect a rise in the price of a commodity in the future, its supply will be inelastic. Producers will choose to hoard the commodity to take advantage of higher prices in the future.

Econometrics Tutorials with Certificates

This website contains affiliate links. When you make a purchase through these links, we may earn a commission at no additional cost to you.