Investment decisions of any firm and in the economy as a whole depend on a variety of factors. Investment involves understanding the effects of lags, future expectations and also the risk associated with investments. Generally, theories of investments deal with only some of these factors in an attempt to understand investment decisions. Incorporating the role of risk, market situation and future expectations can prove difficult. However, Tobin’s q theory attempts to take these factors into account.

Tobin introduced q-ratio including average-q and marginal-q in order to explain investment decisions. Moreover, these ratios are applicable to the economy as a whole as well as individual firms’ investment decisions.

Econometrics Tutorials with Certificates

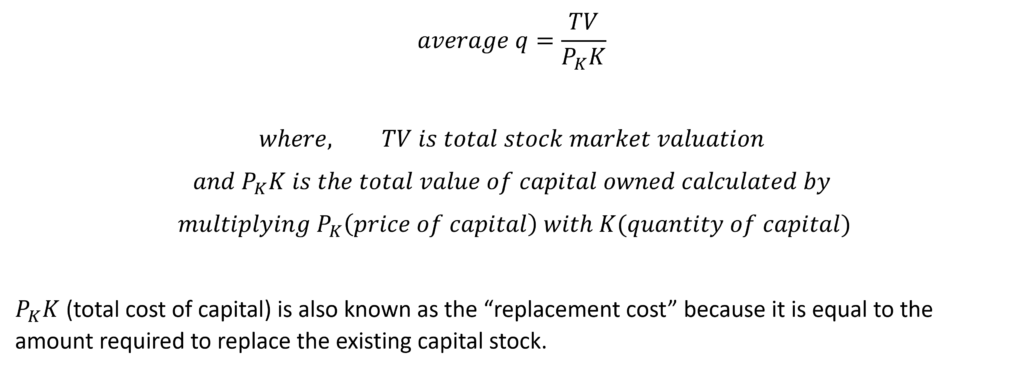

average q

Tobin came forward with a measure known as average-q. Further, it can be estimated as a ratio of total market valuation to the total cost of capital. In the case of a firm, market value will be the total valuation of a firm in the stock market. The total cost of capital will be the value of capital owned by the firm. For the economy as a whole, the total market valuation will be the market value of all the firms in the economy. The total value of capital owned will be the cost of capital. Therefore, the average q can be estimated as:

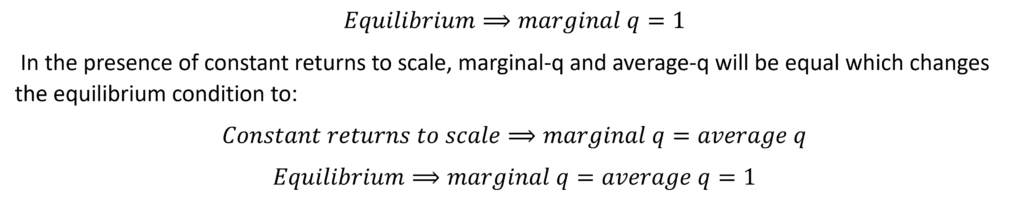

marginal q

Marginal q can be estimated as the ratio of change in total valuation to change in total capital stock. It can also be defined as the increase in market valuation due to an increase in the total cost of capital with a rise in capital stock. Equilibrium is achieved when this marginal-q is equal to one.

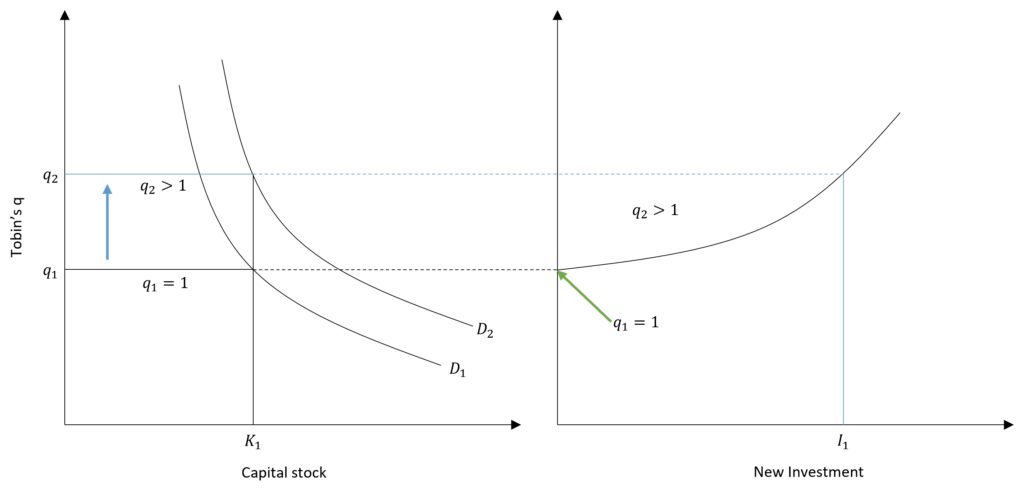

Case 1: Q > 1

Firstly, the investment will increase in the economy or a firm will increase its investment when marginal q is greater than one (q>1). It means that the cost of acquiring capital (PKK) is lower than the market valuation (TV) of the firm or firms. Additional units of capital and investment will lead to a higher increase in total valuation than the increase in replacement costs. That is, the investment pays more than its cost. In such a situation, firms will be induced to invest more.

In the diagram, new investment will start to occur when the value of q rises above q1 because it will increase the demand for capital by shifting D1 to D2.

Case 2: Q < 1

In this second case, the cost of capital is higher than the total market valuation. Hence, firms will reduce their capital stock through disinvestment or they will let depreciation run its course to reduce capital. Also, firms operating with q less than one will be bought by other firms because it is cheaper to buy such firms at a reduced valuation than to buy the same capital which has a higher replacement cost (PKK).

Short-run effect

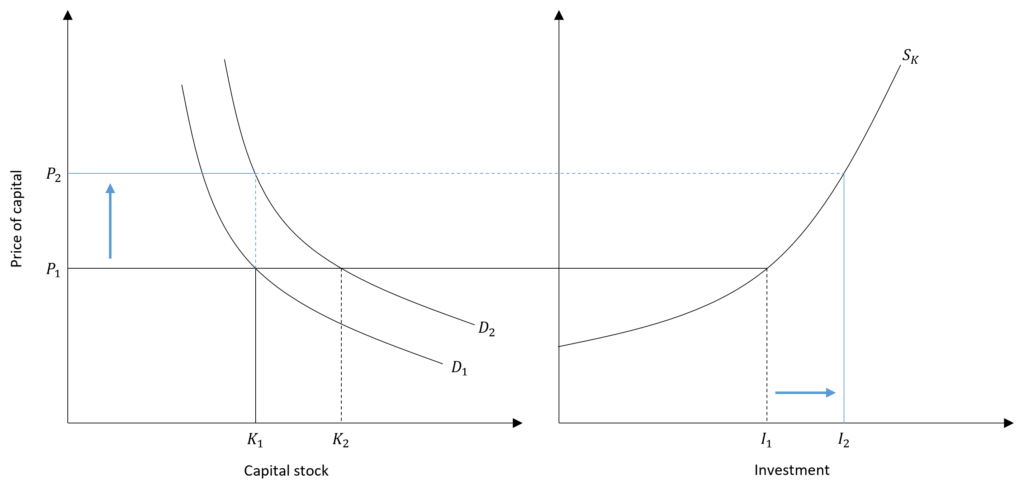

Q value greater than one leads to a shift in demand for capital from D1 to D2. With this shift, the desired capital stock increases from K1 to K2 because of the shift in demand. However, capital stock cannot be increased in the short run. As a result, the price of capital will rise from P1 to P2 with capital stock constant at K1 in the short run. The increase in investment is shown by the movement from I1 to I2.

Capital will increase over a number of time periods to reach the desired capital stock.

advantages and criticism

Advantages

- If a firm knows the replacement cost of capital, the average q can be directly calculated by observing the stock market value of the firm. This makes it easily applicable.

- The observed market value of firms automatically accounts for future expectations, expected returns and risks involved.

- Similarly, market value also allows for lags and adjustment costs in investment.

The market automatically adjusts for these factors and there is no need to make assumptions about future expectations or risks.

Criticism

- Estimating replacement costs can prove to be problematic to calculate average and marginal q. This is because information about the total cost of capital of a firm is not easily available.

- The relation between average and marginal q can be very complex. The assumption of constant returns to scale is unrealistic in this case and both of these measures can be very different and even move in opposite directions.

- The value of q cannot be accurately predicted because stock markets are inefficient. The market valuations may not be accurate and can move erratically.

Econometrics Tutorials with Certificates

This website contains affiliate links. When you make a purchase through these links, we may earn a commission at no additional cost to you.