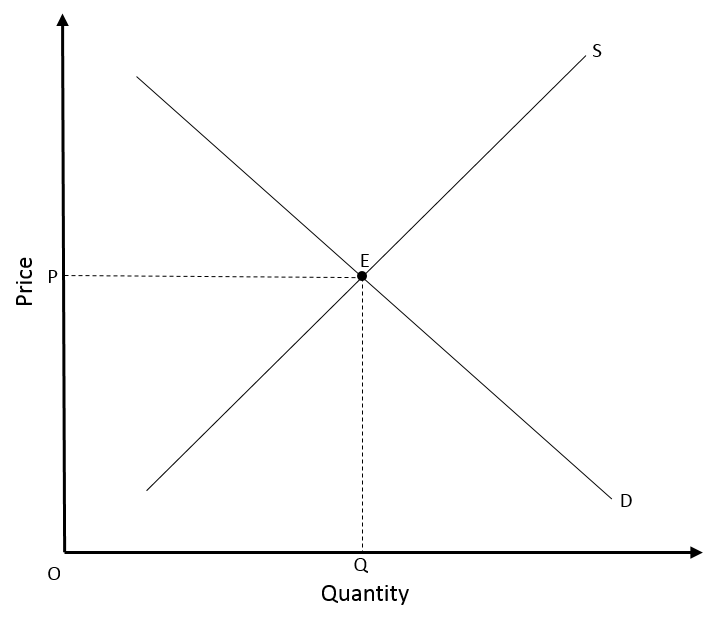

Market equilibrium is a situation where the quantity demanded of a commodity is equal to its quantity supplied. The price and quantity associated with this equilibrium are known as equilibrium price and equilibrium quantity.

In other words, equilibrium price can be defined as the level of price where the quantity demanded of a commodity by consumers is the same as the quantity that producers are willing to sell in the market. This amount of commodity corresponding to equilibrium price is known as equilibrium quantity.

Econometrics Tutorials with Certificates

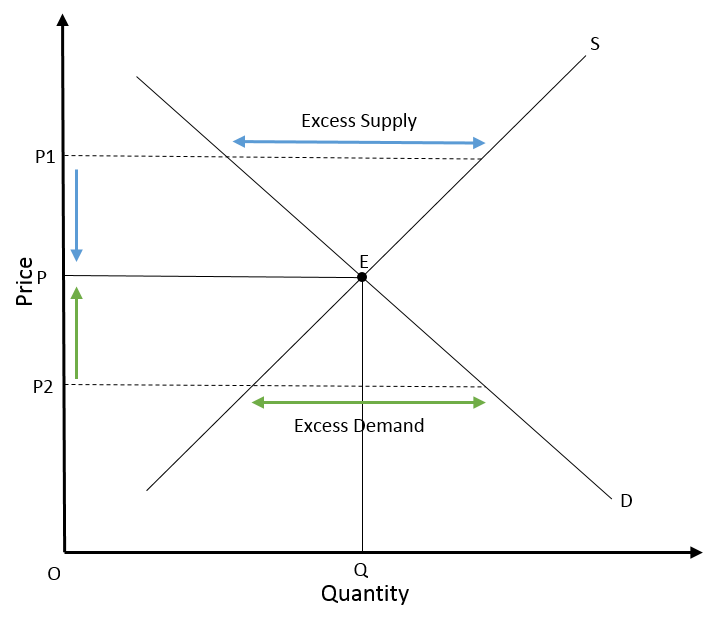

Stable equilibrium

Suppose there is a rise or fall in price leading to excess supply or demand due to any reason. This equilibrium will be automatically corrected by the market forces.

Suppose the price rises to P1. The producers will offer more for sale but the quantity demanded by consumers will decline. This will lead to excess supply or surplus of commodity. To get rid of this excess stock, producers will have to reduce the price which will increase the quantity demanded. Price will continue to fall till it reaches P and equilibrium will be restored.

On the other hand, let the price falls to P2 for some reason. It will create a situation of excess demand or shortages. Consumers will be willing to buy the commodity at higher prices. This will drive the price upwards to P and equilibrium will be restored at quantity Q.

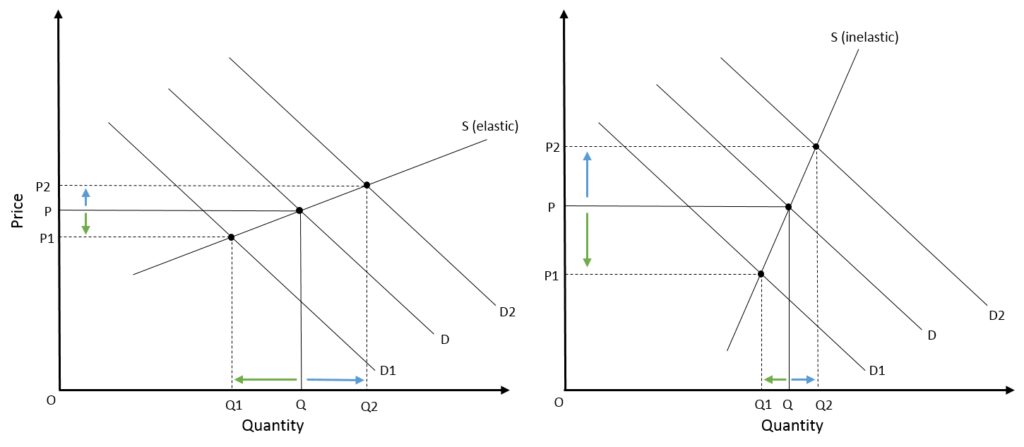

Shifts in demand and role of elasticity

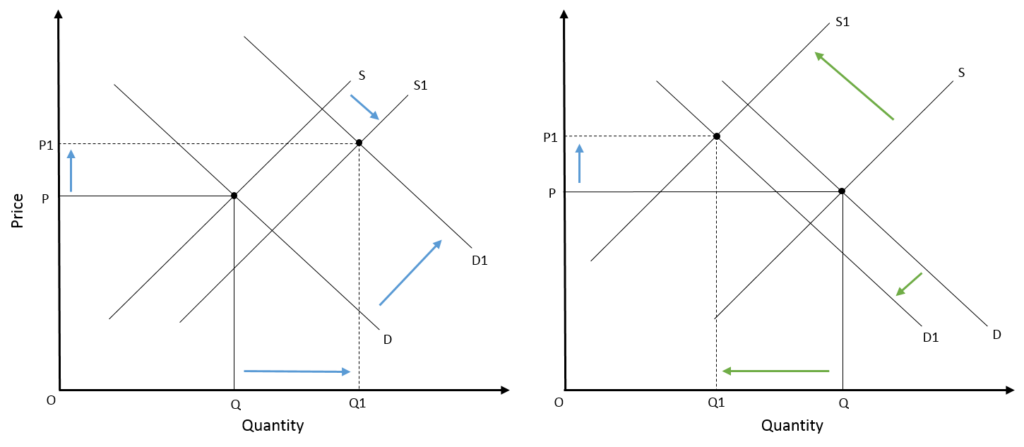

Shifts in demand occur due to changes in factors other than price. For instance, changes in income, prices of related goods and other determinants of demand can shift the demand curve. The determinants of demand are discussed here.

Supply remaining constant, let us assume that the demand curve shifts to the left from D to D1. The equilibrium price (P to P1) and equilibrium quantity (Q to Q1) of the commodity will fall. Conversely, a rightward shift in the demand curve will increase the price from P to P2 and increase the quantity from Q to Q2.

However, the magnitude of increase or decrease in equilibrium price will depend on the elasticity of supply or the nature of the good. An inelastic supply curve will cause a bigger change in equilibrium price as compared to a change in equilibrium quantity. The rise or fall in price is much larger in figure 2 than in figure 1. Hence, a relatively elastic supply curve will be accompanied by a smaller change in equilibrium price as compared to equilibrium quantity.

Durable versus perishable goods: elasticity of supply depends on the nature of the commodity. In the case of durable goods, the elasticity of supply is high. This is because producers can easily store these goods when prices are low and bring them into the market when prices rise. On the other hand, this is not possible for perishable commodities because they cannot be stored for a long period of time. Hence, the change in equilibrium price is greater for perishable goods (inelastic supply) as compared to durable goods (elastic supply), with shifts in demand.

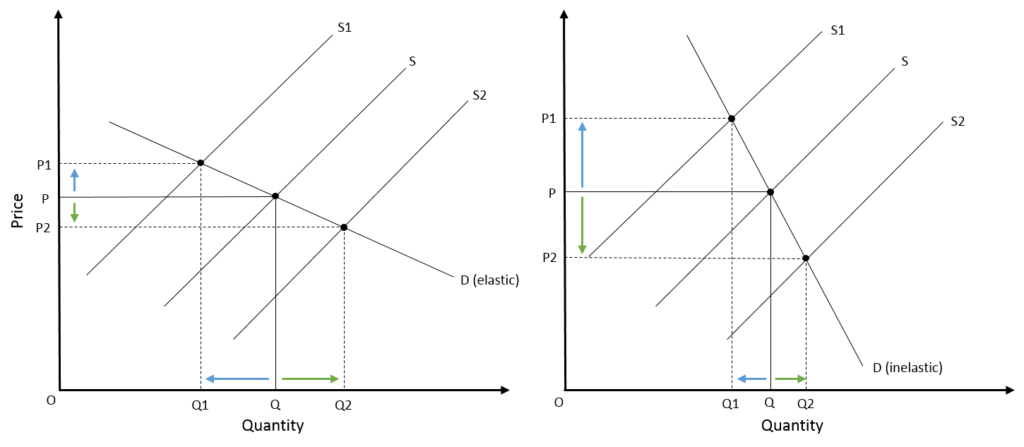

shifts in supply and role of elasticity

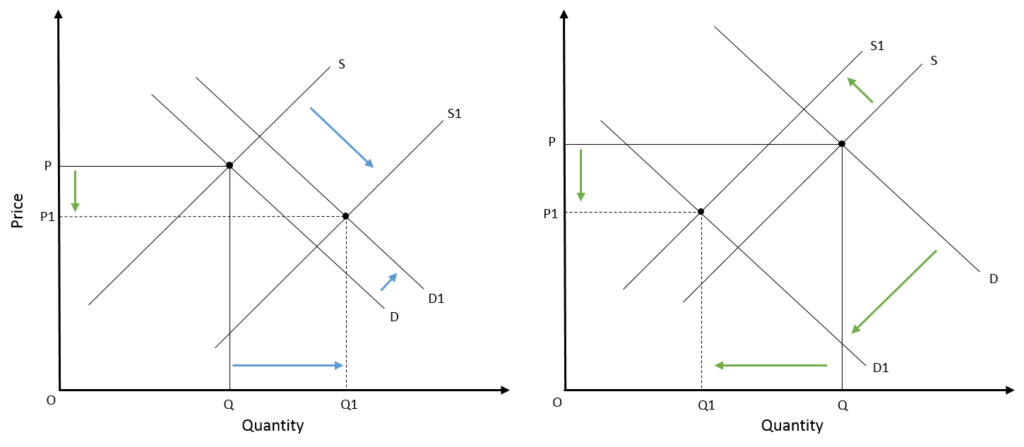

Price being constant, shifts in supply can happen due to other determinants like factor prices.

Demand remaining constant, a shift in the supply curve from S to S1 will cause the equilibrium price to rise and the equilibrium quantity to fall. On the other hand, a rightward shift from S to S2 will lead to a fall in equilibrium price and a rise in equilibrium quantity.

Again, the magnitude of the rise or fall in both equilibrium price and quantity depends on the elasticity of demand. If the demand curve is more inelastic as in the case of figure 2, the change in equilibrium price is greater as compared to change in equilibrium quantity. Hence, an elastic demand curve will have a smaller change in equilibrium price and a larger change in equilibrium quantity with shifts in the supply curve.

Necessities versus luxuries: necessities have a relatively inelastic demand as compared to luxuries. This is because consumers have to purchase a certain minimum amount of necessary goods. Therefore, their demand is less responsive to changes in price. With shifts in supply, change in equilibrium price will be greater for necessities as compared to luxuries. The elasticity of demand is relatively lower or inelastic for necessary goods. In other words, the magnitude of rise or fall in equilibrium price is greater for necessities (inelastic demand) as compared to luxuries (elastic demand), with shifts in supply.

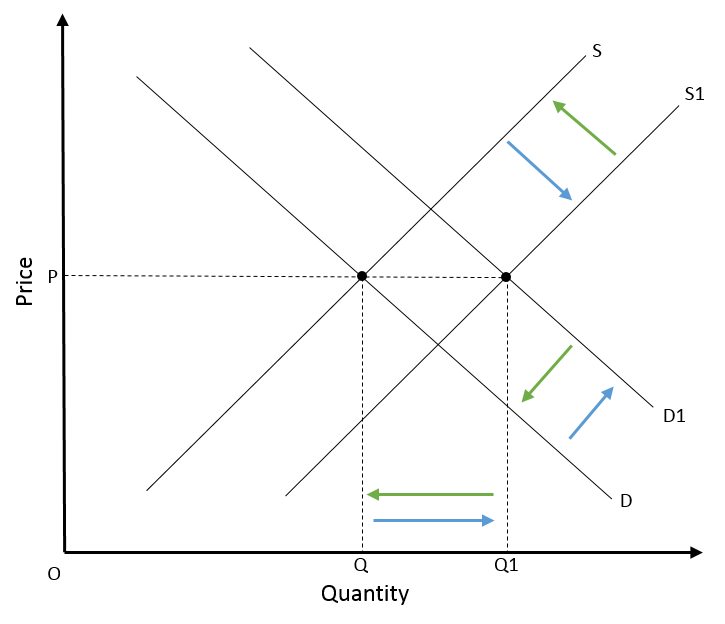

simultaneous shifts in demand and supply

Equilibrium Price remains constant

The equilibrium price will remain the same and the equilibrium quantity will rise with a proportionate rightward shift in demand and supply. That is when the shift in supply is equally proportional to the shift in demand. With a proportionate leftward shift in demand and supply, equilibrium quantity will fall and equilibrium price will remain the same.

Rise in Equilibrium Price

The equilibrium price will rise (P to P1) when the rightward shift in demand is greater than the rightward shift in supply. Similarly, equilibrium price will rise if the leftward shift in supply is greater than the leftward shift in demand.

Fall in Equilibrium Price

Suppose the rightward shift in supply is greater than the rightward shift in demand. Then, the equilibrium price will fall (P to P1). Similarly, when the leftward shift in demand is greater than the leftward shift in supply, the equilibrium price will fall.

Econometrics Tutorials with Certificates

This website contains affiliate links. When you make a purchase through these links, we may earn a commission at no additional cost to you.