The Nationalisation of Banks in India refers to the significant policy move undertaken by the Indian government in 1969 and subsequently in 1980. The move aimed to bring the majority of the banking sector under state control. This decision’s primary objectives were to channel credit towards priority sectors, ensure broader access to banking services, and also promote socioeconomic development by reducing regional disparities.

Before the nationalisation of banks, the Indian banking sector was predominantly controlled by private entities. It led to issues such as limited credit availability to certain sectors, regional imbalances, and exploitation of customers through high interest rates and unfair practices.

Econometrics Tutorials with Certificates

First Phase of Nationalisation (1969)

In July 1969, the Indian government, under the leadership of Prime Minister Indira Gandhi, nationalised 14 major private banks. These banks collectively held around 85% of the total banking assets at that time. The rationale behind this move was to mobilize resources for national development and to ensure credit flow to the priority sectors such as agriculture, small-scale industries, and exports. This move significantly expanded the government’s role in the banking sector. Further, the nationalized banks became instrumental in financing various government-sponsored development programs.

Second Phase of Nationalisation (1980)

The second phase of nationalisation of banks occurred in April 1980, under the government of Prime Minister Indira Gandhi. This time, six more banks were nationalized, bringing the total number of nationalized banks to 20. Same as before, the focus remained on furthering the objectives of social control and directing credit towards priority sectors. With this phase, the government aimed to strengthen the role of banks in rural and agricultural financing and to enhance financial inclusion.

List of Nationalised Banks in India

| Nationalisation of Banks in 1969 | Nationalisation of Banks in 1980 |

| 1. Allahabad Bank (later Indian Bank) 2. Bank of Baroda 3. Bank of India 4. Bank of Maharashtra 5. Canara Bank 6. Central Bank of India 7. Dena Bank (later Bank of Baroda) 8. Indian Bank 9. Indian Overseas Bank 10. Punjab National Bank 11. Syndicate Bank (later Canara Bank) 12. UCO Bank 13. Union Bank of India 14. United Bank of India (later Punjab National Bank) | 1. Andhra Bank (later Union Bank of India) 2. Corporation Bank (later Union Bank of India) 3. New Bank of India (later Punjab National Bank) 4. Oriental Bank of Commerce (later Punjab National Bank) 5. Punjab & Sind Bank 6. Vijaya Bank (later Bank of Baroda) |

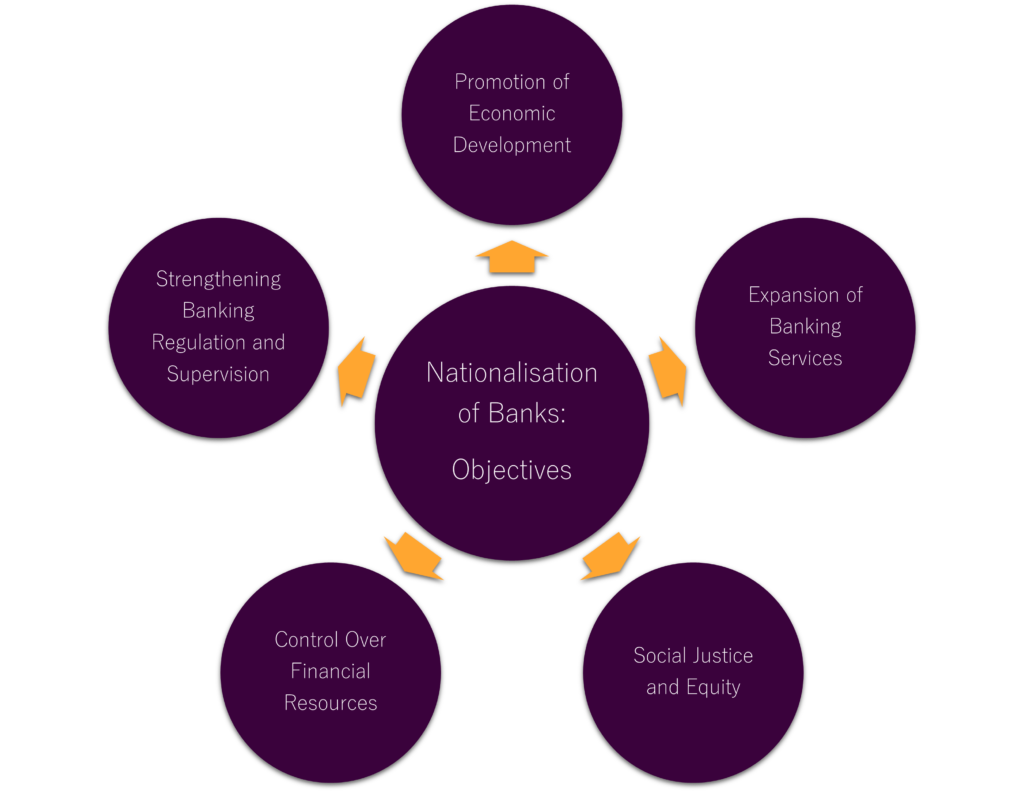

nationalisation of banks: objectives

Promotion of Economic Development

One of the central objectives of the nationalisation of banks was to mobilize financial resources and channel credit towards priority sectors of the economy, such as agriculture, small-scale industries, and infrastructure. By nationalising banks, the government aimed to ensure that these sectors received adequate funding. This was crucial for further stimulating economic growth, creating employment opportunities, and reducing poverty.

Expansion of Banking Services

Another important objective was to expand the reach of banking services, particularly in rural and underserved areas. Before the nationalisation of banks, the banking sector in India was largely concentrated in urban centres. It catered primarily to the needs of industrial and commercial activities. Hence, nationalisation aimed to democratize access to banking services and promote financial inclusion by establishing branches in rural areas and providing banking facilities to unbanked populations.

Social Justice and Equity

Nationalisation of banks was also driven by broader social objectives, such as reducing income inequalities, promoting social justice, and empowering marginalized communities. By bringing banks under state control, the government sought to democratize access to credit and financial resources. This was particularly true for farmers, small entrepreneurs, and economically disadvantaged groups. Therefore, this was seen as a means to address the socioeconomic disparities prevalent in Indian society and promote inclusive development.

Control over Financial Resources

Nationalisation enabled the government to exert greater control over financial resources and leverage them for national development goals. By owning a majority stake in banks, the government could further influence lending policies, direct credit flow towards priority sectors, and finance government-sponsored development programs. This control was deemed necessary to ensure that banking resources were utilized in alignment with the country’s developmental priorities.

Strengthening Banking Regulation and Supervision

Nationalisation also aimed to strengthen regulatory oversight and supervision of the banking sector. By consolidating the banking industry under state control, the government could also enact and enforce prudential regulations, safeguard depositor interests, and maintain stability in the financial system. Nationalized banks were subject to stricter regulatory standards. Hence, they were expected to adhere to prudent banking practices to ensure the safety and soundness of the banking system.

Positive Impact of nationalisation of banks

Expansion of Branch Network

The Nationalization of banks led to a significant expansion of the branch network, particularly in rural areas. According to the Reserve Bank of India (RBI), the number of bank branches increased from 8,262 in 1969 to 59,635 in 2019, reflecting a more than sevenfold increase. This expansion helped improve access to banking services for millions of people across the country. (Source: RBI Handbook of Statistics on Indian Economy)

Increased Deposit Mobilization

Nationalised banks played a crucial role in mobilizing deposits from various segments of society, including rural households, small savers, and low-income earners. Data from the RBI shows that total deposits in the banking system increased from Rs. 5,970 crore in 1969 to Rs. 140.6 lakh crore in 2020, therefore, indicating a substantial growth in deposit mobilization over the years. (Source: RBI Handbook of Statistics on Indian Economy)

Credit Flow to Priority Sectors

Nationalisation helped direct credit towards priority sectors such as agriculture, small-scale industries, and exports. These sectors were also crucial for economic development and poverty reduction. According to the RBI, the share of priority sector advances in total bank credit increased from 16.4% in 1969 to 40.2% in 2020, highlighting the enhanced focus on priority sector lending by nationalized banks. (Source: RBI Handbook of Statistics on Indian Economy)

Promotion of Financial Inclusion

Nationalized banks played a pivotal role in promoting financial inclusion by providing banking services to previously unbanked and underserved populations. According to the World Bank’s Global Findex database, the percentage of adults with an account at a financial institution increased from 35% in 2011 to 80% in 2017, indicating a significant improvement in financial inclusion driven by initiatives of nationalized banks and government policies. (Source: World Bank Global Findex Database)

Support for Small-Scale Industries

Nationalised banks also extended credit support to small-scale industries, contributing to their growth and employment generation. Data from the Ministry of Micro, Small & Medium Enterprises (MSMEs) shows that the number of registered MSMEs increased from 11.33 lakh units in 1969 to 6.33 crore units in 2020, reflecting the significant expansion of the sector supported by bank financing.

Reduction in Regional Disparities

Nationalisation helped reduce regional disparities by ensuring the availability of banking services in remote and backward regions. Therefore, the presence of nationalised banks in rural areas led to improved access to credit, increased investment, and reduced income disparities between rural and urban areas.

Stability in the Financial System

Nationalized banks also contributed to the stability of the financial system by adhering to prudential norms and maintaining sound banking practices. Despite periodic challenges, such as non-performing assets (NPAs), nationalized banks have played a crucial role in maintaining financial stability and preventing systemic risks.

Support for Government Programs

Nationalized banks have been instrumental in financing various government-sponsored programs aimed at poverty alleviation, rural development, and social welfare. Moreover, these programs have benefited millions of households by providing access to banking services and credit facilities.

Innovation in Banking Products

Nationalized banks have introduced innovative banking products and services to cater to the diverse needs of customers, including digital banking, mobile banking, and online payment solutions. These technological advancements have further enhanced customer convenience, improved operational efficiency, and promoted financial literacy and inclusion.

Contribution to Economic Growth

Overall, nationalized banks have made a significant contribution to India’s economic growth and development by mobilizing financial resources, promoting investment, and supporting entrepreneurship and innovation. Studies have shown a positive correlation between the presence of nationalized banks and economic growth indicators such as GDP growth, employment generation, and poverty reduction.

Negative Impact of nationalisation of banks

Operational Inefficiencies

Nationalized banks often face challenges in operational efficiency and productivity due to bureaucratic procedures, political interference, and lack of autonomy. Nationalized banks often exhibit lower levels of efficiency and profitability compared to private banks, which hinder their ability to compete effectively in the market.

Credit Misallocation

Despite the intention to prioritize lending to priority sectors, nationalized banks sometimes misallocated credit due to political pressure or bureaucratic decision-making. This further resulted in the inefficient use of resources and reduced effectiveness in achieving development goals. Instances of politically motivated lending by nationalized banks often lead to loan defaults and further financial losses.

Rise in Non-Performing Assets (NPAs)

Nationalised banks have historically struggled with high levels of non-performing assets (NPAs), which are loans that have stopped generating income for the bank due to defaults or delays in repayment. According to data from the Reserve Bank of India (RBI), nationalized banks accounted for a significant portion of the total NPAs in the banking sector, therefore, reflecting weaknesses in credit risk management and asset quality.

Limited Innovation and Adaptation

Nationalised banks have also been criticized for their slow pace of innovation and adaptation to changing market dynamics, including technological advancements and customer preferences. Nationalized banks in India have lagged behind their private counterparts in adopting digital banking solutions and improving customer service. This has further affected their competitiveness and customer satisfaction.

Resource Misallocation

Nationalization led to a concentration of financial resources in the hands of the government, which sometimes also resulted in misallocation and inefficient use of funds. Studies have shown that nationalized banks often directed credit towards politically connected borrowers or inefficient projects, rather than sectors with high economic potential or social impact. This led to suboptimal outcomes in terms of economic growth and development.

Crowding Out of Private Sector

The dominance of nationalised banks in the banking sector also crowded out private banks and non-banking financial institutions, limiting competition and innovation. The presence of large state-owned banks in India have often crowded out private sector credit, particularly in sectors where government-owned banks had a dominant market share.

Political Interference

Nationalized banks have been susceptible to political interference, including pressure to lend to politically connected borrowers or support government priorities at the expense of commercial viability. Hence, this interference compromised the autonomy and independence of bank management and undermined market discipline and accountability. Reports by regulatory authorities and independent watchdogs have further highlighted instances of political meddling in the operations of nationalized banks.

Loss of Market Discipline

Government ownership of banks sometimes led to a loss of market discipline, as investors and creditors perceived state-owned banks as implicitly backed by the government, leading to moral hazard and risk-taking behaviour. A study published in the Journal of Financial Economics found evidence of moral hazard in nationalized banks, as they engaged in riskier lending practices and took on excessive leverage due to the perception of government support. (Source: “Market Discipline and the Use of Government Bonds as Collateral in the Eurozone” – Journal of Financial Economics)

Decline in Customer Service Quality

Nationalized banks have been criticized for their poor customer service quality, including long wait times, bureaucratic procedures, and lack of responsiveness to customer needs. Surveys conducted by consumer organizations and market research firms have consistently rated nationalized banks lower in terms of customer satisfaction compared to private banks, reflecting deficiencies in service delivery and customer-centricity.

Financial Burden on Government

Nationalized banks have sometimes become a financial burden on the government, requiring periodic capital infusions and bailouts to shore up their capital adequacy and solvency. The allocation of public funds to recapitalize nationalized banks diverts resources from other priority areas such as infrastructure, education, and healthcare, imposing fiscal constraints on the government and reducing its ability to invest in long-term development initiatives.

Econometrics Tutorials with Certificates

This website contains affiliate links. When you make a purchase through these links, we may earn a commission at no additional cost to you.

Good to see a such a precise article ,

Thank you!!!