Empirical studies and observations exposed the shortcomings of the absolute income hypothesis. It failed to explain the patterns of consumption over a long period of time. It did not consider the role of business cycles or wealth as a factor in determining consumption. As a result, several other theories emerged which attempted to explain the behaviour of consumption, such as the Permanent Income Hypothesis.

Permanent income and consumption

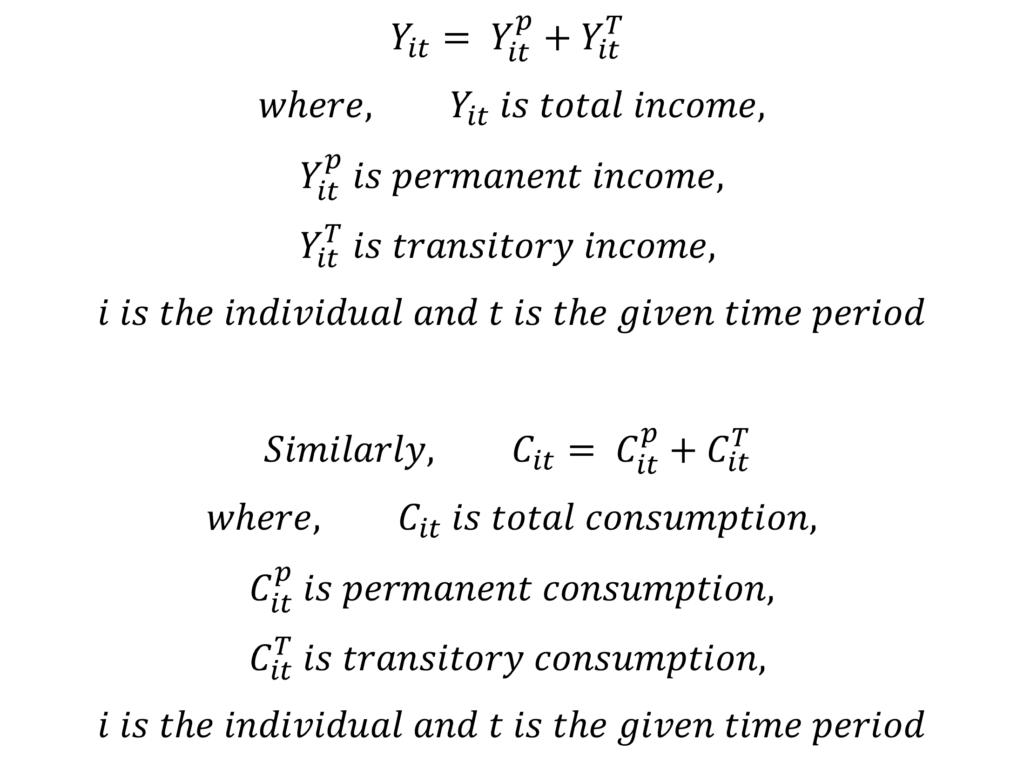

The permanent income hypothesis was introduced by Milton Friedman. It is based on the assumption that individuals aim for utility maximization. According to Friedman, permanent consumption is a function of the permanent income of a consumer.

Here, “theta” explains the proportion of permanent income used in permanent consumption, which turns out to be simply the ratio of permanent consumption to the permanent income of the consumer. The actual value of this ratio depends on several factors including the rate of interest, tastes and preferences of the given consumer and expected income.

Relationship between permanent and total income/consumption

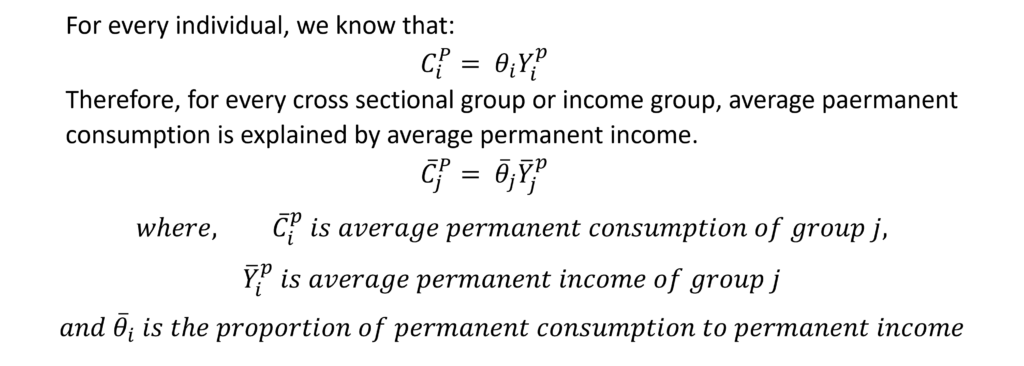

This permanent income and permanent consumption are different from total income and total consumption in a given time period. The relationship between these can be illustrated as follows:

The transitory income and transitory consumption are random deviations from permanent income and permanent consumption respectively, which leads to differences in total income and consumption. This transitory income and consumption can be positive, negative or zero. The sum of transitory and permanent elements makes up the total income and consumption in a given time period for each individual.

assumptions made by Friedman

Friedman made some assumptions about all the above components and the way they are related to each other. These assumptions help explain the behaviour of consumption and can be stated as follows:

- There is no relationship between transitory income and permanent income. Hence, total income fluctuates randomly around the permanent income with zero covariance between the total and permanent income of different individuals.

- Similarly, there is no correlation between transitory consumption and permanent consumption. Total consumption is a random fluctuation around permanent consumption. Therefore, the covariance between total and permanent consumption is zero.

- There is no relationship between transitory income and transitory consumption. The covariance of transitory income and transitory consumption is zero. This is true because Friedman includes the purchase of non-durable goods only and not the purchase of durable goods in consumption. The usage of durable goods is included in consumption through depreciation. Therefore, if consumers purchase durable goods from transitory income, it does not have a significant effect on consumption because only usage of durables is included in consumption, not their purchase.

Empirical Evidence and explanation using Permanent Income Hypothesis

MPC < APC in cross-sectional studies

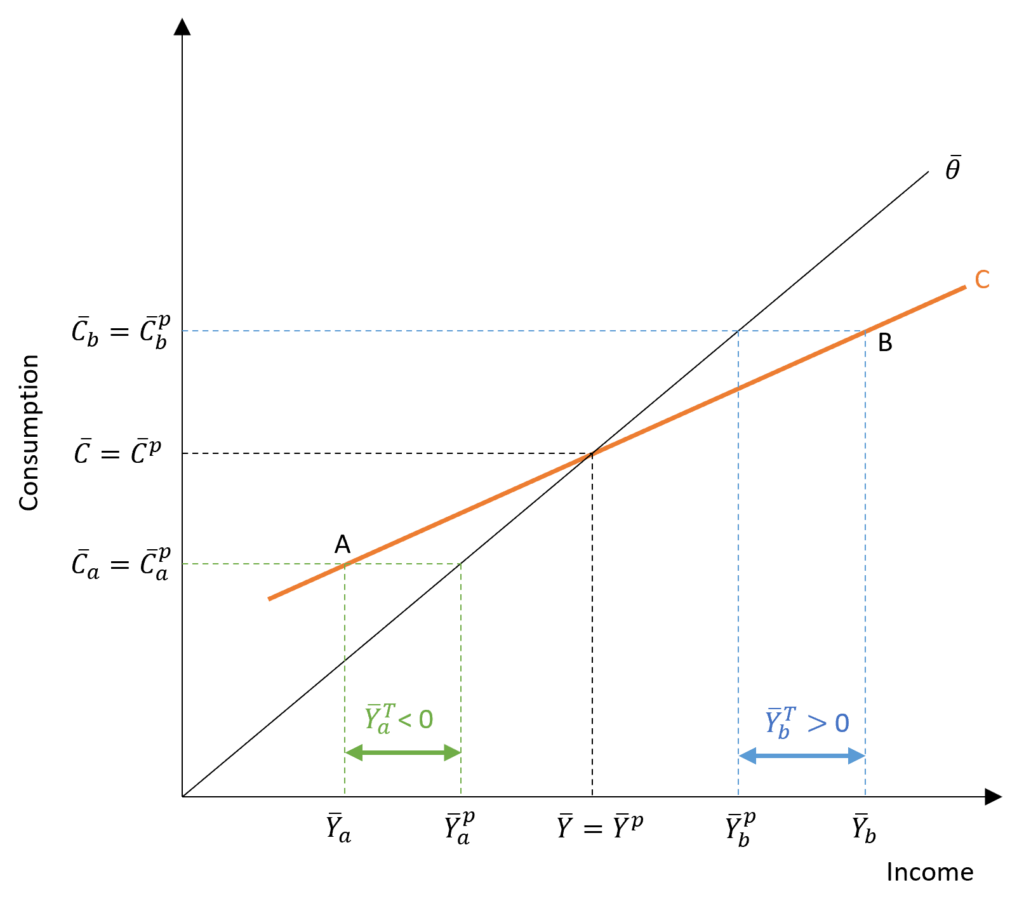

However, transitory consumption has no relationship with transitory income or permanent consumption. The average transitory consumption of every income group will be zero. As a result, average permanent consumption will be equal to average total consumption in every income group.

An income group ‘b’, which has an average income higher than the average population income, will have a positive average transitory income. That is, the average permanent income of that group will be less than the average total income. This difference is equal to the value of average transitory income. Since the average transitory consumption will be zero, the average permanent and average total consumption of group ‘b’ will be equal. It is shown by point “B” in the diagram.

On the other hand, income group ‘a’ has a negative average transitory income implying that the average permanent income is greater than the average total income in that case. The average total and average permanent consumption will be equal, corresponding to point A.

Similarly, the income group with an average income equal to the average population income has zero transitory income. At this point, the average permanent income is equal to the average total income of the group.

Cross-sectional consumption function

This gives rise to the cross-sectional consumption function which is shown by ‘C’. In the case of high-income group ‘b’, APC is observed at point B. Point B lies below the population consumption line, hence, APC at point B is less than the overall APC of the population which is equal to theta. Conversely, APC at point A corresponding to group ‘a’ lies higher than the population consumption line. APC is greater than the constant APC of the population (theta). Hence, APC is falling as we move from low to high-income groups and MPC<APC on the consumption function ‘C’. The slope of the cross-sectional consumption function is less than the population consumption line.

As the economy grows and average permanent income rises for all groups, this consumption function ‘C’ keeps shifting upwards along the trend, which is the population consumption line. In the long run, the observed consumption function is the population consumption line of “theta” with a constant APC.

Long-run and cyclical fluctuations

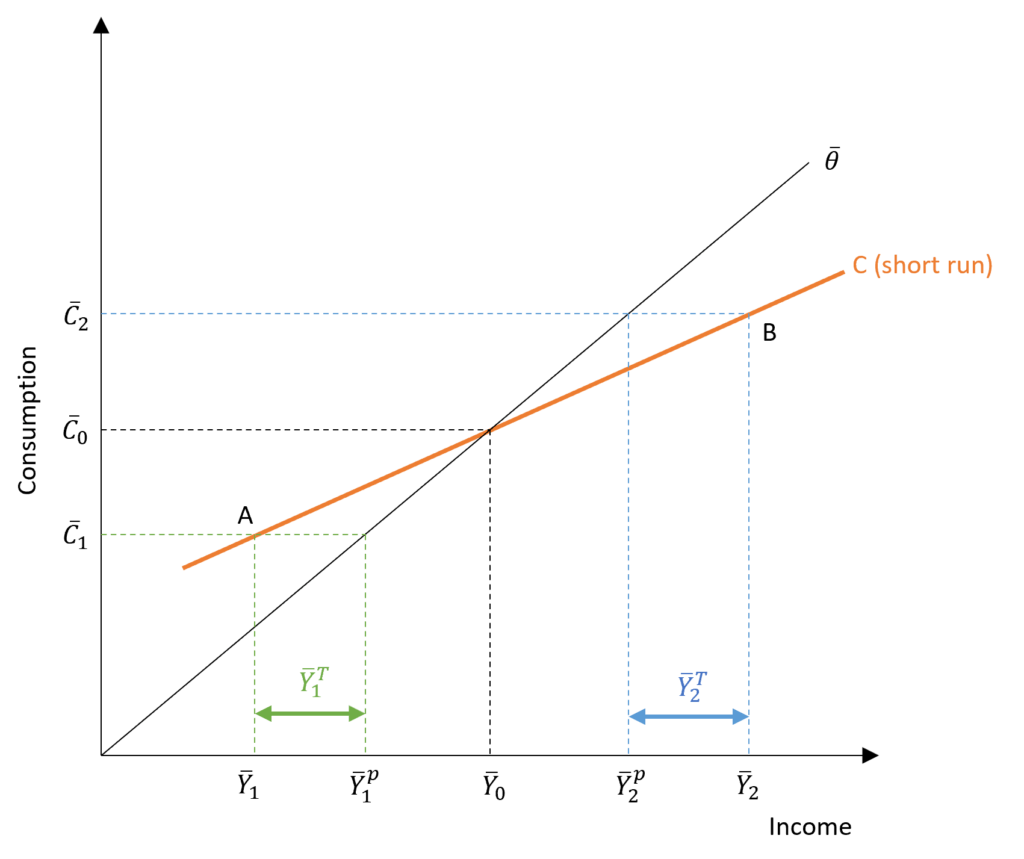

The explanation of consumption over a long run and short run fluctuation due to business cycles is similar to that of cross-sectional groups.

Instead of the high-income group, we have a period of boom in the economy at point B when the average transitory income is positive. The average permanent income is, therefore, less than the average total income in the economy. On the opposite end, we have a period of slump in the economy at point A. Average transitory income is negative and average permanent income is greater than the average total income in the economy.

These points A and B corresponding to periods of slump and boom, show us the short-run consumption function ‘C’. At point A, APC is greater than long-run APC (theta) and APC at point B is less than long-run APC. Therefore, MPC < APC in the short run corresponds to each business cycle when the slope of ‘C‘ is less than the trend line. The long-run consumption is shown by the trend line with APC = MPC at constant theta. This trend line or long-run permanent consumption is observed over a long period as the economy grows and the short-run consumption function goes on shifting upwards.

determining permanent income: adaptive expectations

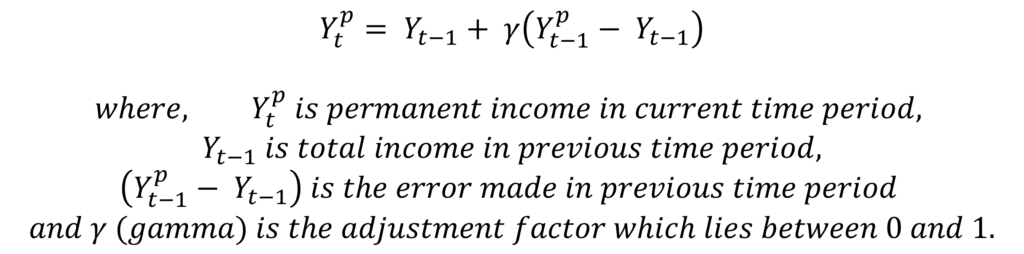

This approach by Friedman divides total income into permanent income and transitory income. In reality, these two components are not observed separately, but, only the total income is observed. Therefore, Friedman used the method of adaptive expectations to separate permanent income from transitory income. Using adaptive expectation, permanent income can be extracted from total income in actual time series data as follows:

Therefore, if gamma is closer to zero, it implies that we are giving less weightage to the last period error (transitory income) and relying more on the actual income in the previous time period. On the contrary, if gamma is close to 1, we are giving high weightage to the error in determining permanent income. At gamma = 0, we completely ignore the past error. At gamma = 1, we don’t change expectations at all as we assume error will be exactly the same as last period.

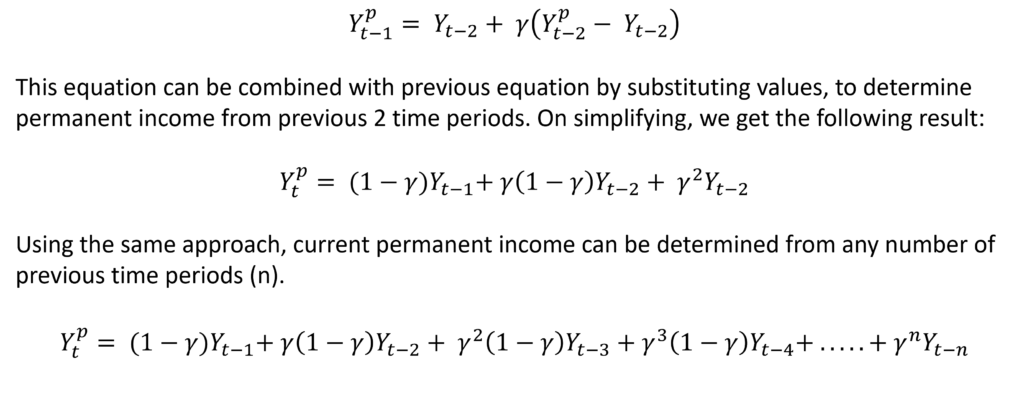

The above equation shows that the permanent income in the current period depends only on past incomes. Similarly, permanent income in the previous time period (t-1) can be expressed as follows:

criticism of Permanent Income Hypothesis

- It does not explicitly account for wealth or the role of assets. It implicitly includes assets as part of consumption through the ‘usage’ of assets, measured by depreciation and rate of interest.

- In adaptive expectations, only previous period income is used to determine current permanent income. Whereas, income is a function of many factors apart from previous incomes.

- It includes the consumption of durables only through depreciation and rate of interest. The purchase of durables from transitory income or windfall gains is not considered.

- The theory assumes APC to be constant at “theta” while estimating permanent consumption. However, it does not have to be constant even within an income group. APC is expected to fall as income increases because lower-income groups have to spend a greater portion of their income to meet their needs.