If a non-stationary time series has to be differenced “d” times to make it stationary, that time series is integrated of order “d”. In other words, the order of integration tells us the number of times a non-stationary time series must be differenced to make it stationary. Furthermore, it is generally denoted as “I(d)”.

This type of time series is known as an integrated process. Random Walk Model without drift is one example of an integrated process. We have also seen the nature of non-stationarity in the Random Walk Model. We observed that it becomes stationary at first difference. This implies that the time series is integrated of order 1 and is written as I(1).

If a time series becomes stationary at the second difference, then it is referred to as being Integrated of order 2 and is expressed as I(2).

Econometrics Tutorials with Certificates

Determining the order of integration of a time series

The Augmented Dickey-Fuller Test (ADF) is commonly used to determine the order of integration of a time series. The basic idea is to test for the level of difference that the series is stationary at. If the time series is stationary at level or as it originally is, then it is integrated of order 0. If the time series becomes stationary at the first difference, it is integrated of order 1. Therefore, in this way, we go on differencing the time series till it becomes stationary and we determine the order of integration.

It is important to note here that the ADF test is not the only test that we can use for this purpose. Several other tests such as the KPSS, Phillips Perron, DF-GLS etc. can be employed here.

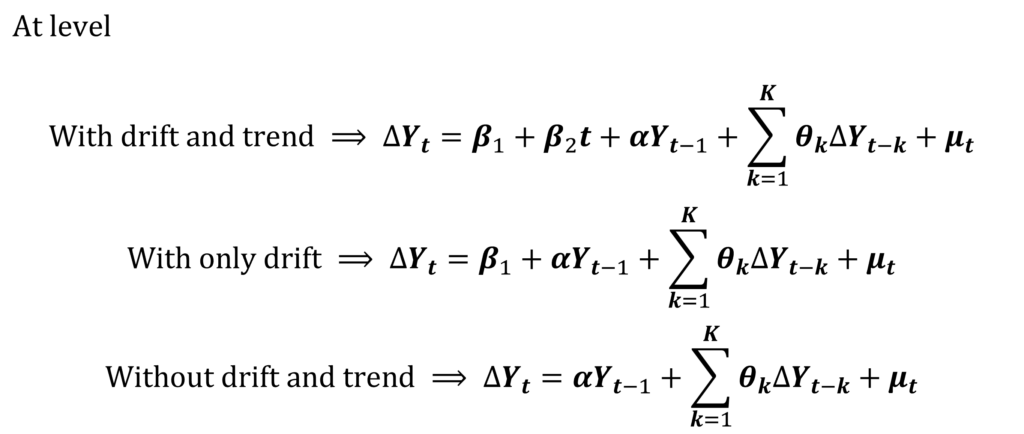

Similar to what we discussed in the post on the ADF test, we have to apply the test to 3 equations:

- With drift and trend

- With only drift

- Without drift and trend

Stationary at level: Order of integration is I(0)

Initially, we will have to test for stationarity at level. This is similar to testing whether the series is I(0). We will use the ADF test to determine this using the following equations:

If the trend is significant, we have to use the first equation with drift and trend. When the trend is insignificant, we estimate the second equation with only the drift component. In case both trend and drift are insignificant, then we move on to the third equation without drift and trend.

After deciding the appropriate equation to use and estimating it, we can interpret the results. The coefficient associated with Yt-1 (that is, α) tells us about the stationarity of the time series and its order of integration:

- α is negative and significant = stationary at level and the time series is I(0)

- α is positive or insignificant = non-stationary at level and try first difference

In practice, the results of the test will be similar to the following:

| ADF test statistic | -1.068 | p-value = 0.1436 |

| Critical Value at 5% | -1.655 | |

| Coefficient | p-value | |

| Yt-1 | α = -0.0008 | 0.287 |

| Drift | β1 = 0.174 | 0.013 |

The above table shows the results of the ADF test applied to a time series. We can observe that the time series is non-stationary at level. This is evident because the coefficient “α” is negative but insignificant and the p-value of the ADF test statistic is greater than 0.05. Hence, this means that the time series is not I(0). Moreover, we have used the second equation with only the drift component because the trend was insignificant.

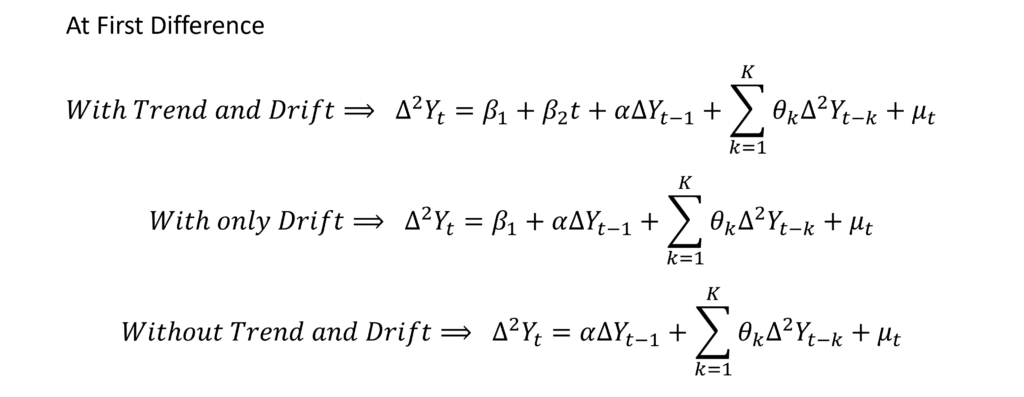

Stationary at First Difference: Order of integration is I(1)

We observed above that the time series is non-stationary at level. Therefore, we take the first difference of the series and apply the ADF test:

Here, we have adapted the equations of the ADF test for the first difference of the series. The procedure of application and its interpretation, however, remains the same. Finally, let us look at the results:

| ADF test statistic | -5.845 | p-value = 0.0000 |

| Critical Value at 5% | -1.655 | |

| Coefficient | p-value | |

| ∆Yt-1 | α = -0.5549 | 0.000 |

| Drift | β1 = 0.0103 | 0.000 |

After taking the First difference, the trend was insignificant again. Therefore, we estimated the second equation with only drift. Since drift is significant, we can use this equation to interpret the results. The coefficient “α” is negative and significant along with a significant ADF test statistic. This implies that the time series is stationary at first difference. In other words, the time series is Integrated of Order 1 or I(1).

Suppose, the test still showed that the time series is non-stationary. Then, we take the second difference of the time series and apply the ADF test again. We can keep on going with this procedure till we figure out the order of integration of the series.

Related Posts

- Stationarity and Stationary Time series

- ADF test

- Random Walk Model

- Dickey Fuller test of stationarity

- Interpreting ACF and PACF plots

Econometrics Tutorials with Certificates

This website contains affiliate links. When you make a purchase through these links, we may earn a commission at no additional cost to you.