The trickle-down economics or trickle-down effect posits that tax incentives and benefits for the affluent will trickle down to benefit society at large. Hence, this strategy advocates for reduced regulations and lower taxes for the wealthy, aiming to stimulate economic growth. It further suggests that retaining more corporate funds will spur business investments, technological advancements, and job creation.

However, detractors contend that this strategy exacerbates income disparities and may not effectively stimulate the economy. The efficacy of trickle-down economics remains a pivotal topic in economic policy discussions, with both supporters and critics passionately debating its advantages and disadvantages.

Econometrics Tutorials with Certificates

Understanding the Trickle-Down Economics

Key Economic Principles and Core Assumptions

The “trickle-down effect” rose to fame in the 1980s, linked to the economic strategies of the Reagan administration in the U.S.

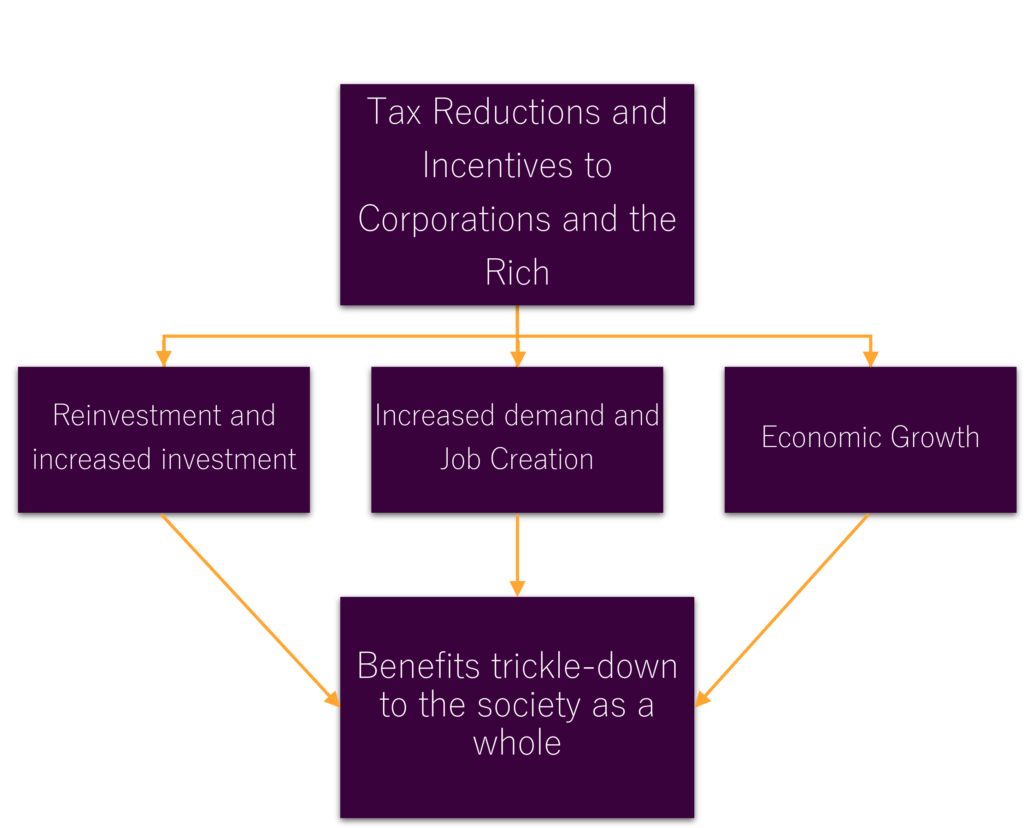

Trickle-down economics posits that tax reductions for the affluent and corporations will spur economic growth, also benefiting society as a whole. Hence, its core tenets include slashing corporate income taxes, reducing tax brackets for the wealthy, and deregulating to boost investment and business growth.

The trickle-down effect hinges on the notion that wealth redistribution to the affluent will trickle down to the lower and middle classes through job creation, increased spending, and economic expansion. It also posits a hierarchical society where the lower classes aspire to the lifestyles and consumption patterns of the wealthy, driving economic growth.

How Trickle-Down Economics Works in Practice

The core premise of trickle-down economics centers on the implementation of tax cuts, primarily targeting high-income earners and corporations. It posits that such tax breaks will lead to increased corporate investment, job creation, and ultimately higher wages for workers. That is, the benefits are expected to “trickle down” to the broader population.

Tax Policy Implementation

Trickle-down economics advocates for reducing marginal income tax rates. Lowering the tax burden on the wealthy and businesses, therefore, leads to additional capital being reinvested. This is further believed to generate economic growth and job opportunities.

Corporate Benefits and Investment

Proponents of trickle-down economics argue that tax cuts for corporations and high-income individuals will also spur investment. This, therefore, will lead to job creation and higher wages. However, critics contend that the wealthy may choose to save rather than spend their additional income. This limits the intended trickle-down effect.

Wealth Distribution Mechanisms

The trickle-down theory also suggests that the increased spending and investment by the wealthy will create demand for goods and services. This, in turn, is expected to lead to the creation of new businesses and job opportunities. It is believed that this will result in a more equitable distribution of wealth across the income spectrum.

Historical Implementation of Trickle-Down Policies

The concept of “trickle-down economics” has been a subject of intense debate and implementation throughout economic history. One of the most notable examples of its application was during the Reagan administration in the 1980s. Ronald Reagan’s Economic Recovery Act of 1981 lowered the top income tax rate from 70% to 50% over 3 years, and even the lowest tax rate was reduced by 3%. The Act also reduced the capital gains tax rate by 8% from 28% to 20%. The Tax Reform Act of 1986 further reduced the top income tax rate from 50% to 28% and increased the lowest tax rate from 11% to 15%.

Modern Applications

The principles of trickle-down economics have resurfaced in more recent times, with the 2017 Tax Cuts and Jobs Act under the Trump administration being a prominent example. A study from the London School of Economics analyzed 18 developed countries over a 50-year period from 1965 to 2015 to compare the effects of tax cuts on the wealthy. The research highlights that while incomes of the rich grew faster in countries with lowered tax rates, the benefits did not trickle down to the middle class, leading to exacerbated income inequality (Source: The Economic Consequences of Major Tax Cuts for the Rich by David Hope and Julian Limberg)

Impact on Income Inequality and Economic Growth

Recent studies have yielded mixed results regarding the impact of trickle-down policies on income inequality and economic growth. A report from the London School of Economics (also mentioned above) found that five decades of tax cuts in 18 wealthy nations primarily benefited the affluent. These policies showed no significant impact on unemployment or economic growth. Critics contend that these benefits to the wealthy can distort the economic structure, exacerbating income disparities.

The trickle-down policies may stimulate investment and economic growth. However, studies suggest that increasing income inequality can hinder investment and diminish growth in economies with weak demand. In advanced economies, income inequality may not spur higher investment but rather slow growth and increase debt.

Critics and Alternative Economic Theories

Critics of trickle-down economics contend that its supposed benefits rarely materialize in reality. They assert that tax cuts and benefits for corporations and the affluent do not necessarily translate into increased investment, job creation, or economic expansion. Instead, these policies are often accused of increasing income inequality. Hence, the wealthy reap the majority of the benefits, widening the wealth gap.

Academic research also supports these criticisms. The study mentioned earlier by the London School of Economics revealed that tax cuts for the affluent did not significantly improve unemployment or overall economic growth.

Contrasting trickle-down economics, alternative theories stress the significance of demand-side factors and progressive taxation for achieving equitable and sustainable economic growth. These models propose that investing in education, infrastructure, and social programs could be more effective in enhancing the living standards of the working and middle classes. This, as a result, drives broader economic expansion.

Advocates of these alternative approaches argue that redistributing wealth more evenly and strengthening the social safety net can lead to economic benefits trickling up to the affluent, rather than relying solely on trickle-down models. They posit that such policies can foster a more balanced and inclusive growth model, addressing poverty and inequality, rather than solely benefiting the wealthy.

Conclusion

The trickle-down economics or effect is a contentious economic theory, with both advocates and detractors voicing their opinions. Proponents suggest that tax cuts for the affluent can spur investment, thereby boosting overall economic growth. Conversely, critics argue that such policies often concentrate wealth at the top, worsening income disparities.

Practical applications of trickle-down policies have shown varied outcomes, with some research indicating minimal benefits for economic expansion and poverty alleviation. A study by the London School of Economics discovered that unemployment rates and GDP per capita were nearly indistinguishable between nations that cut taxes for the rich and those that did not. As the economic environment continues to shift, policymakers and economists are deeply engaged in discussions regarding the efficacy of trickle-down strategies versus alternative models.

Econometrics Tutorials with Certificates

This website contains affiliate links. When you make a purchase through these links, we may earn a commission at no additional cost to you.